Key Events: A heat wave, but a cooling economy

In contrast to the heat wave much of America is suffering through, the economy is cooling:

- The conference board index of leading economic indicators has declined for 15 months.[1]

- Q2 earnings season cooled this week, reflecting the 6th straight quarter of profit margin declines. Earnings are still expected to grow, however, for the full year and in 2024.[2]

- Inflation expectations continue to cool.[3]

Market Review: growth stocks take a pause

Value stocks shined this week as large cap growth was the only style to lose money. The S&P 500 gained 0.7% for the week while small cap value stocks earned 2.1%.

International and emerging market stocks lost money.

Bonds stood still, anticipating the Fed meeting next week.

Outlook: Expecting the Fed too cool off as well

The Federal Reserve meets next week, and the market expects them to announce the final interest rate hike of the cycle. The market expects, in a shift from earlier in the year, that the Fed will not cut rates this year.

This reflects the strengthening of data the market has been processing. High yield bond spreads remain low, indicating the bond market does not expect a recession. This contrasts with economists’ expectations for a recession, illustrated in the chart below.

Listen to our Q3 market update webinar, recorded on July 18, to hear our perspective on the economy and markets.

OneAscent Market Update: Q3 2023

Recession expectations[4]

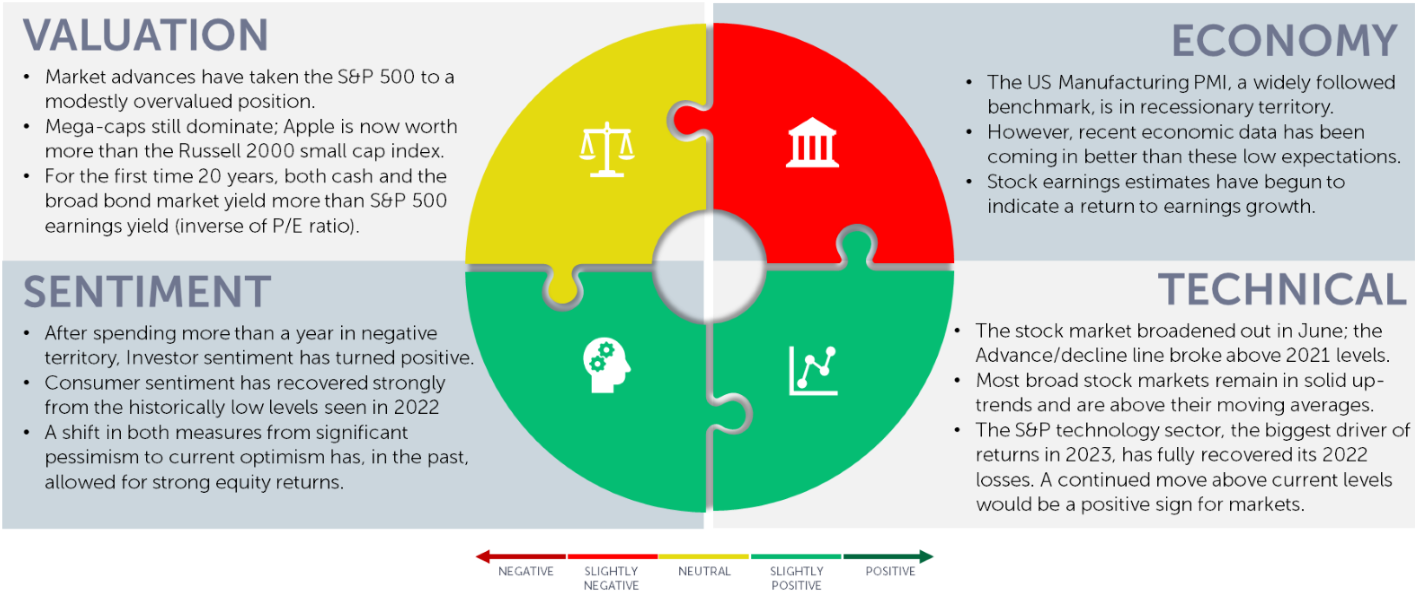

Navigator Outlook: July 2023

This material is intended to be educational in nature,[5] and not as a recommendation of any particular strategy, approach, product or concept for any particular advisor or client. These materials are not intended as any form of substitute for individualized investment advice. The discussion is general in nature, and therefore not intended to recommend or endorse any asset class, security, or technical aspect of any security for the purpose of allowing a reader to use the approach on their own. Before participating in any investment program or making any investment, clients as well as all other readers are encouraged to consult with their own professional advisers, including investment advisers and tax advisors. OneAscent can assist in determining a suitable investment approach for a given individual, which may or may not closely resemble the strategies outlined herein.

[1] Source: The Conference Board Leading Economic Index® US Leading Indicators (conference-board.org)

[2] Source: Factset earnings insight

[3] Source: NY Fed inflation expectations survey – 1-year. Survey of Consumer Expectations – FEDERAL RESERVE BANK of NEW YORK (newyorkfed.org)

[4] Source: Bloomberg

[5] Market Returns reference the following indices: Large Cap – S&P 500, Mid Cap Growth – Russell Midcap growth, Mid Cap Value – Russell Midcap Value, Small Cap – Russell 2000, Developed – MSCI EAFE, Emerging – MSCI Emerging Markets, Aggretate – Bloomberg US Aggregate, High Yield – Bloomberg High Yield

OAI00379